Margins are tightening. Card fees are rising. Legacy payment systems are slowing businesses down. For UK businesses looking to modernise operations and reduce payment friction, Pay by Bank offers a strategic advantage. Built on open banking infrastructure, it allows funds to move directly from customer to business, instantly, securely, and without the cost of card networks or the hassle of outdated terminals.

More than just a payment method, Pay by Bank is fast becoming a default expectation among mobile-first customers and finance-conscious businesses alike. This guide unpacks how it works, where it fits best, and why now is the right time to adopt it.

What is Pay by Bank?

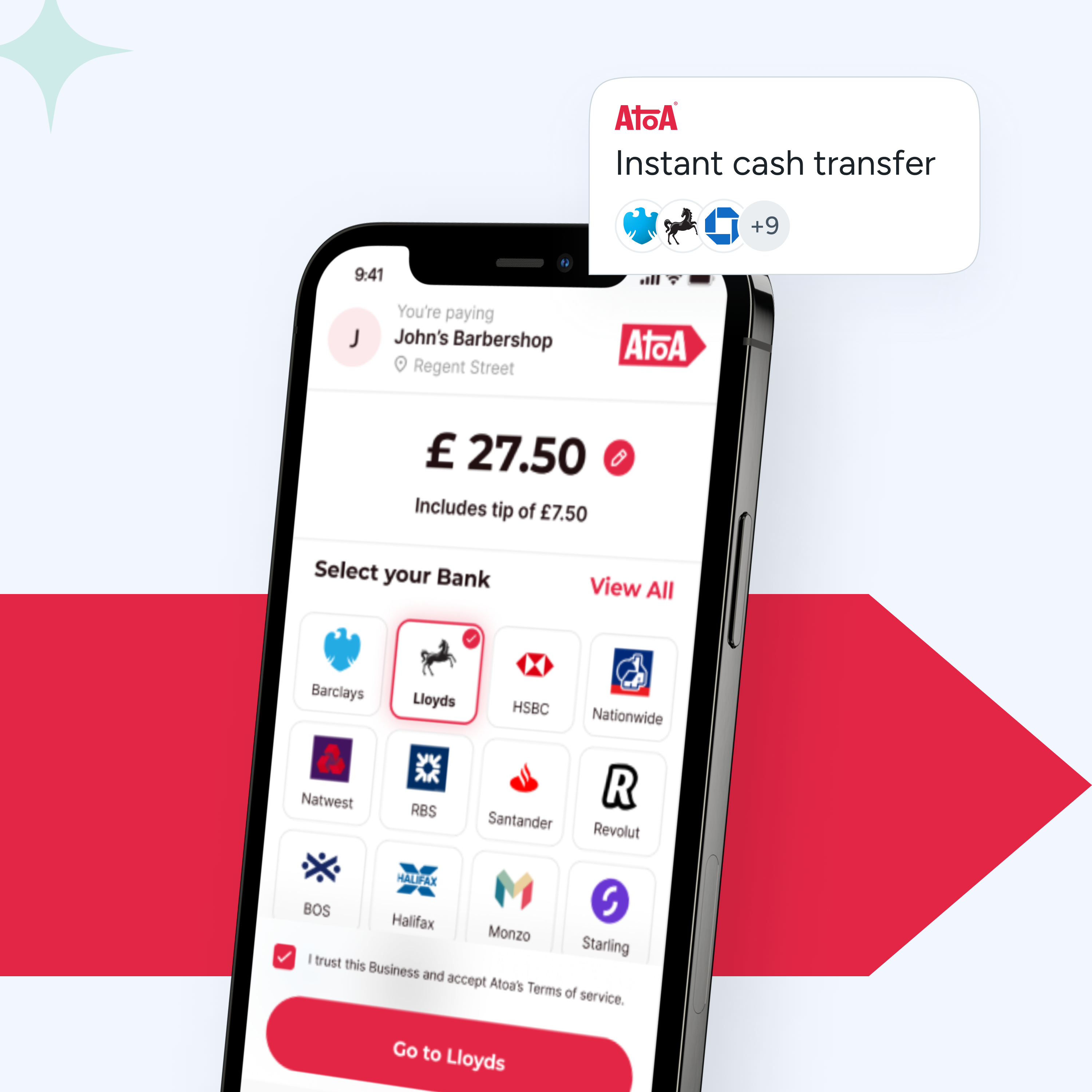

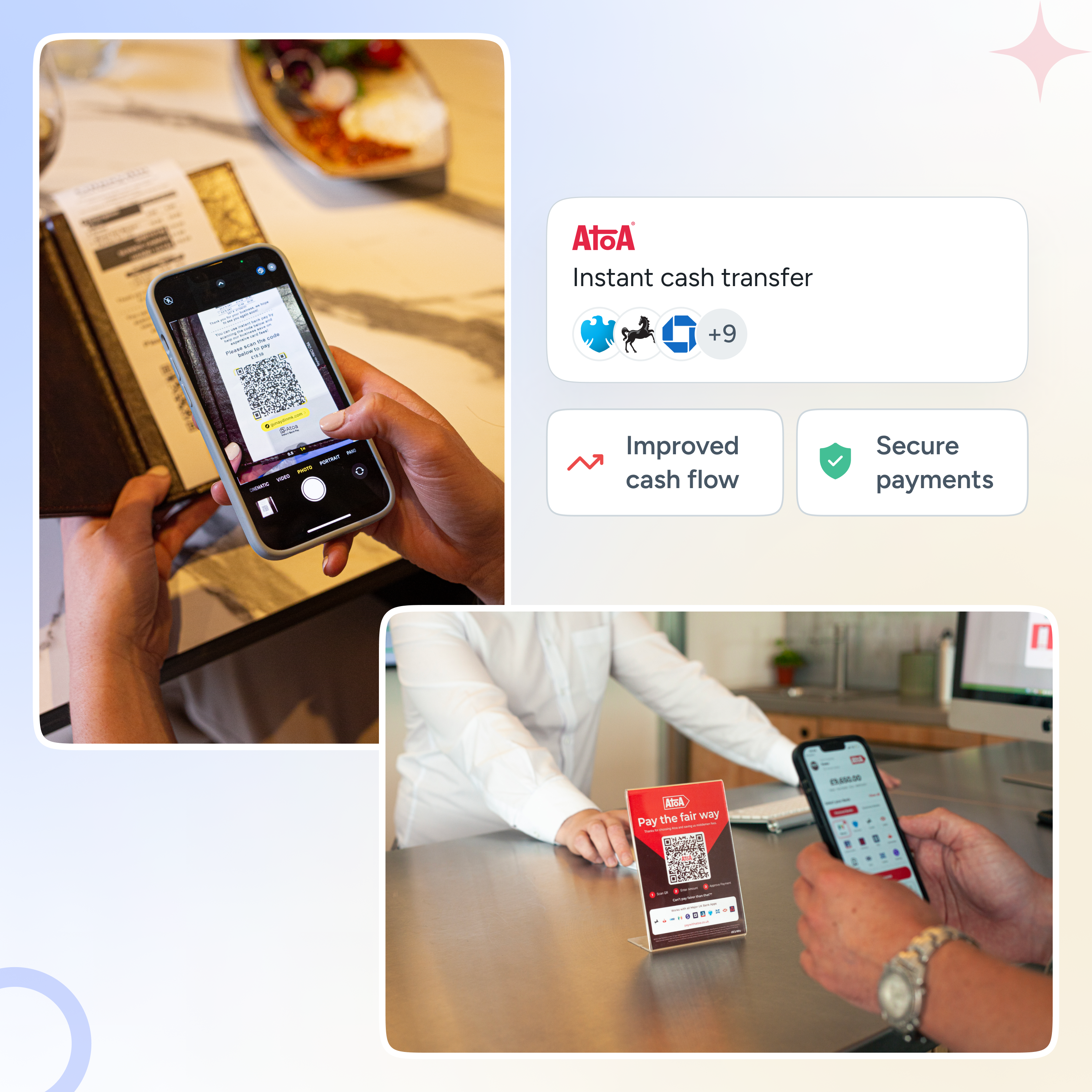

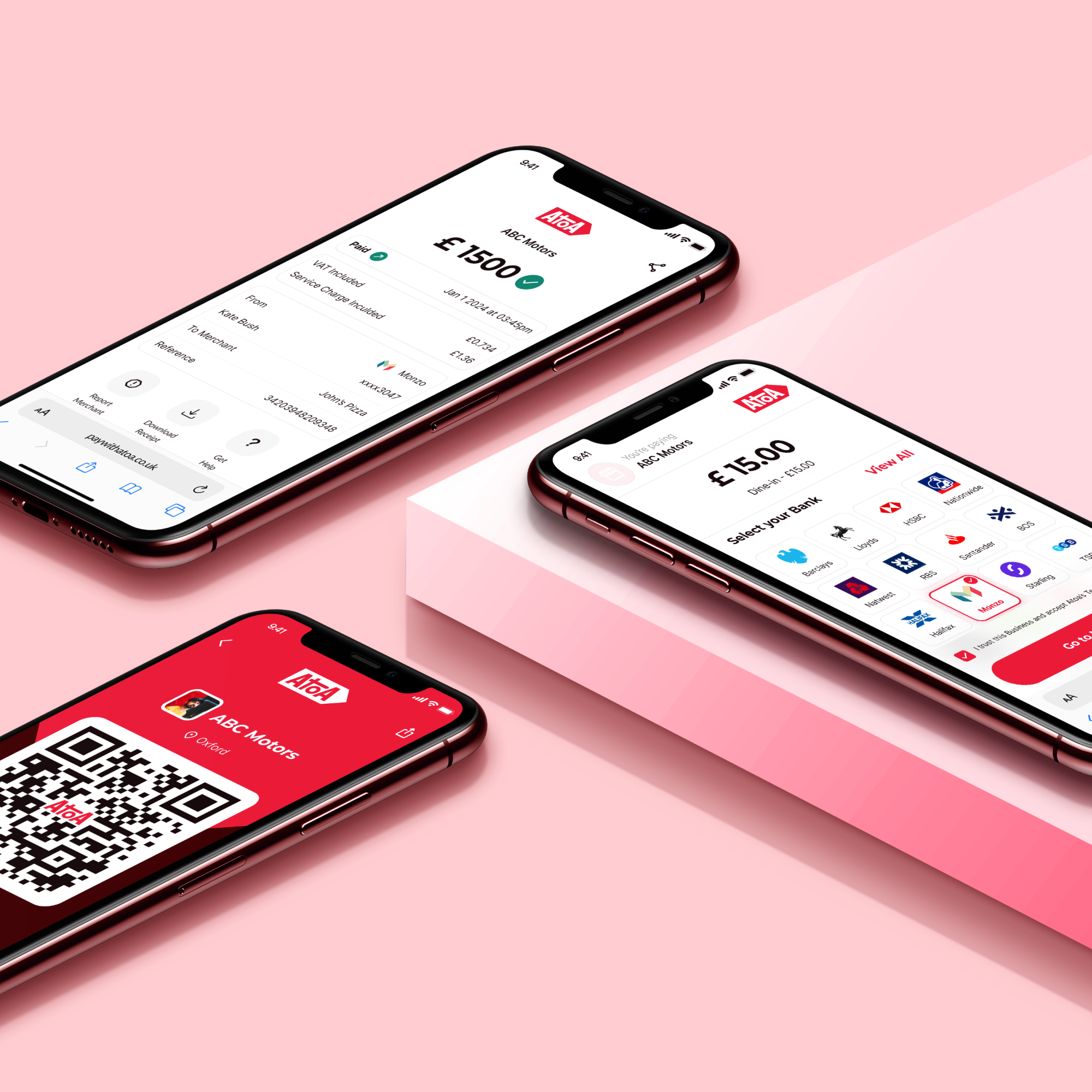

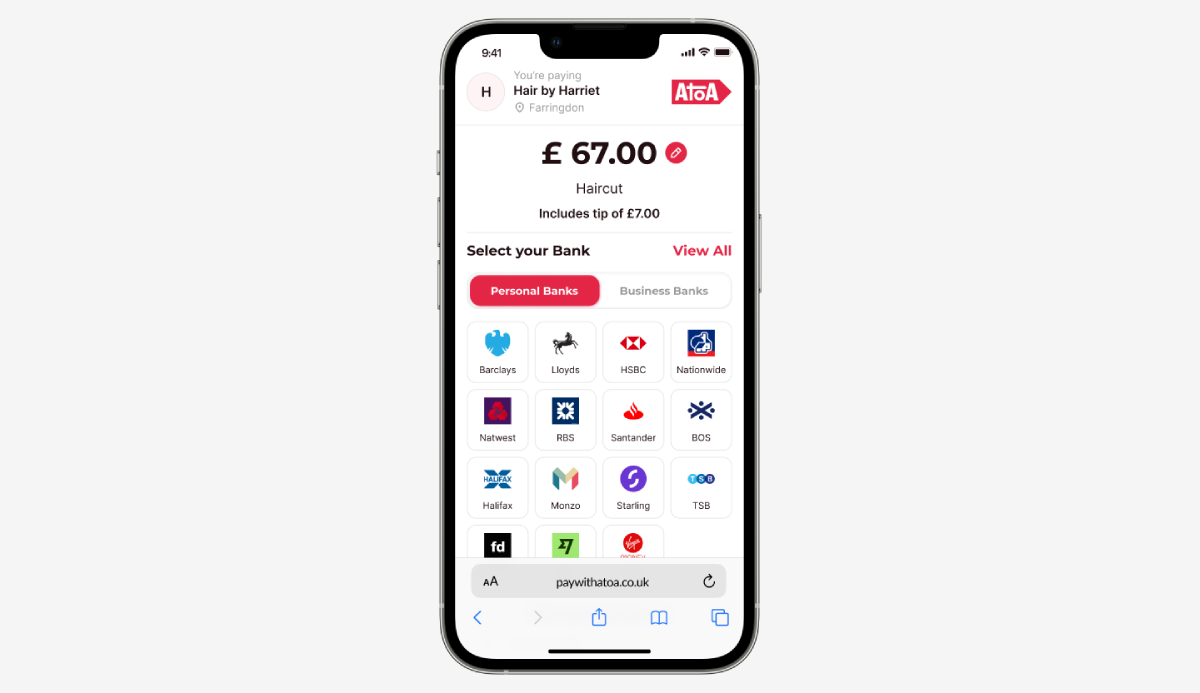

Pay by Bank allows real-time, account-to-account payments without involving card networks like Visa or Mastercard. Instead of typing in long account numbers or waiting days for settlement, customers make payments through their own bank app by tapping a payment link or scanning a QR code. The payment is authorised and transferred instantly, with full visibility and confirmation provided to both parties.

Why it’s better than cards

Card machines have been the default for years, but they come with real costs:

- Transaction fees that add up fast

- Chargebacks that disrupt cash flow

- Hardware and rental fees that eat into margins

Pay by Bank removes the middlemen. You can avoid card fees altogether and get paid instantly, which means your cash flow improves overnight.

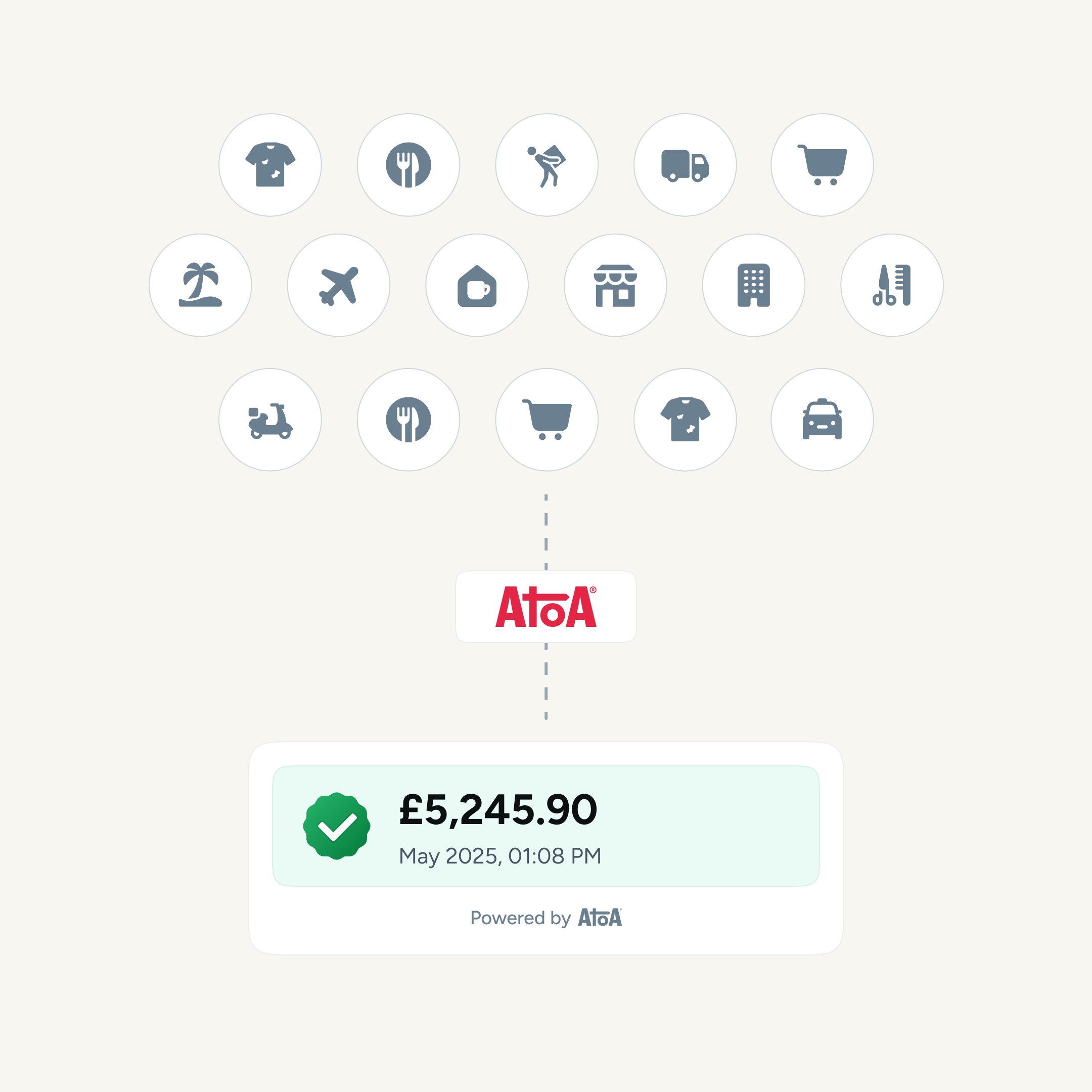

Where Pay by Bank works best

Pay by Bank is quietly transforming payment experiences across industries. Here’s how different sectors are using it as a practical, modern alternative to cards:

- Salons & spas: Businesses in beauty and wellness are using payment links or QR codes to collect deposits or full payments before or after appointments. It helps reduce no-shows and saves time at checkout.

- Car dealerships: Pay by Bank has proven ideal for large-value transactions such as service charges, deposits, or down payments. Instant confirmations, no card limits, and lower fees make it a natural fit for high-ticket sales.

- Law firms: Firms are sending payment links for consultation fees, retainers, or invoice settlements. Payments are trackable, secure, and confirmed in real-time.

Watch how Family Law Cafe uses Atoa and benefits from their payments link feature to collect instant payments.

- Clinics: Many healthcare businesses now let patients pay via QR code at the front desk or by link post-appointment. It’s discreet, fast, and doesn’t require handling cash or cards.

- Retail stores: Retailers are combining Pay by Bank with their POS systems or online checkouts to offer faster payments and smoother reconciliation. It’s especially handy during busy hours when speed matters most.

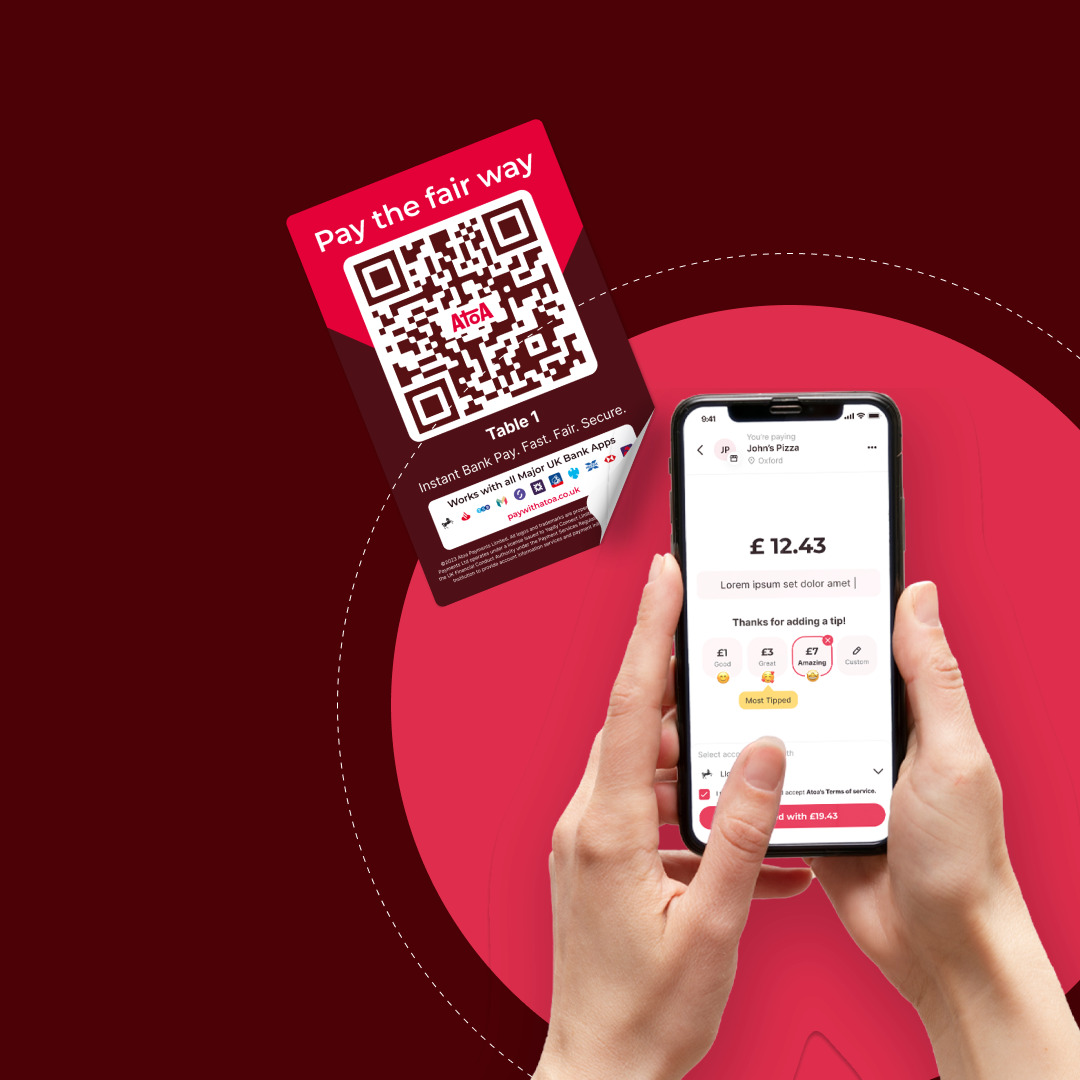

- Restaurant chains: Hospitality businesses are placing QR codes at tables or kiosks, allowing guests to pay when ready. Orders are marked as paid instantly, helping staff manage tables faster and reduce manual errors.

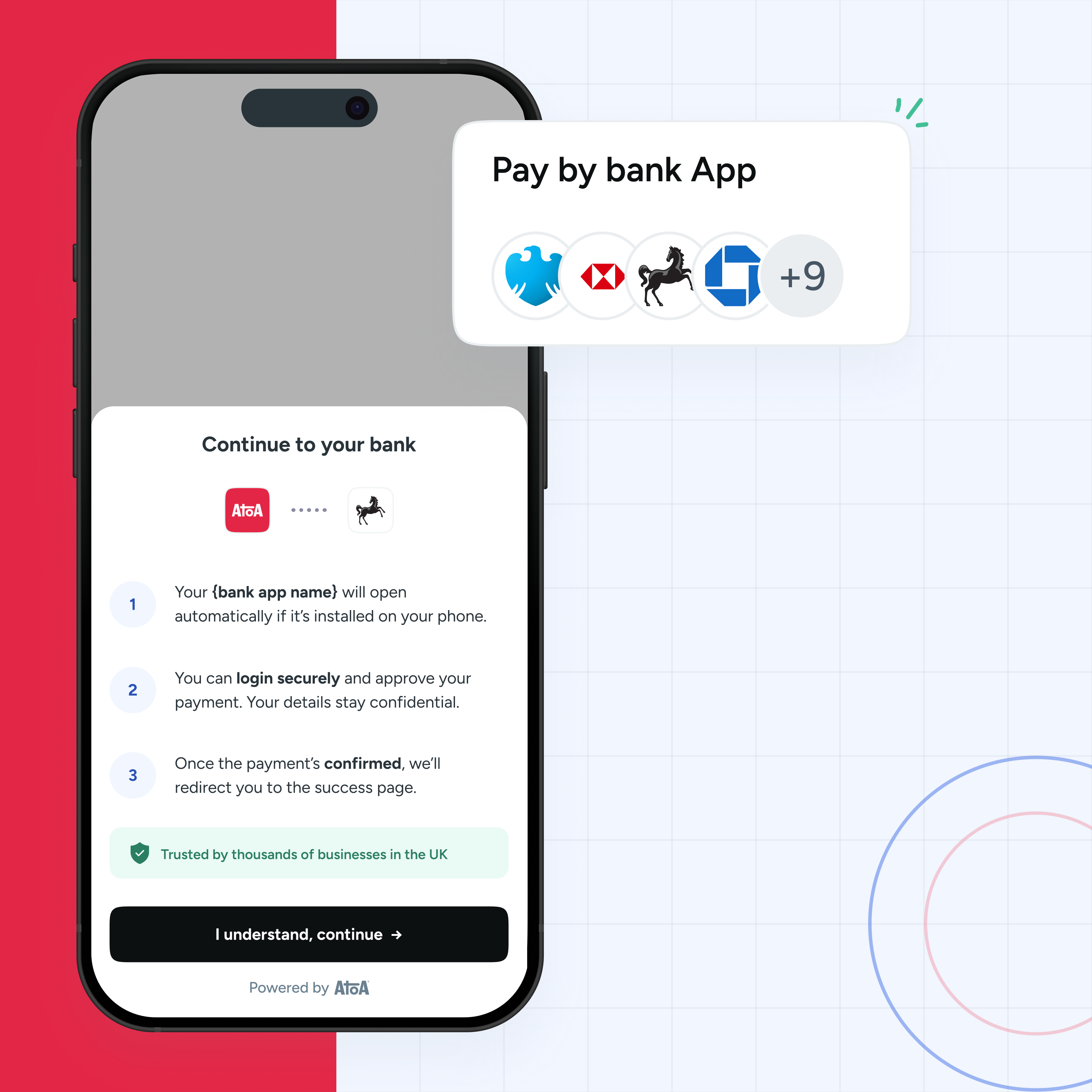

Isn’t this just a bank transfer? Not quite

It’s a common myth, “Isn’t this just like sending an account number?” But Pay by Bank is a major upgrade:

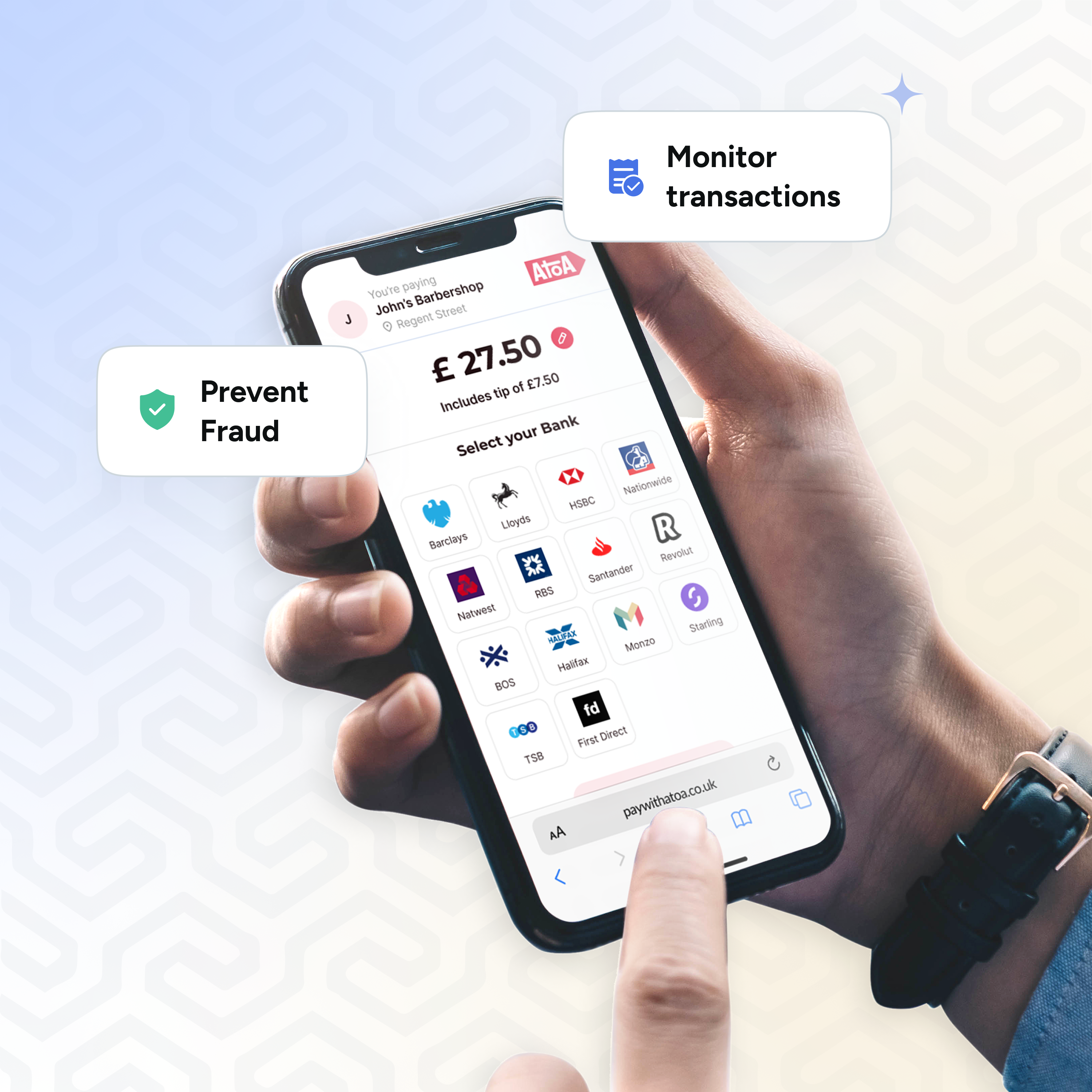

- Strong Customer Authentication (SCA): Customers approve every payment inside their secure banking app.

- No manual entry: No sort codes or account numbers required.

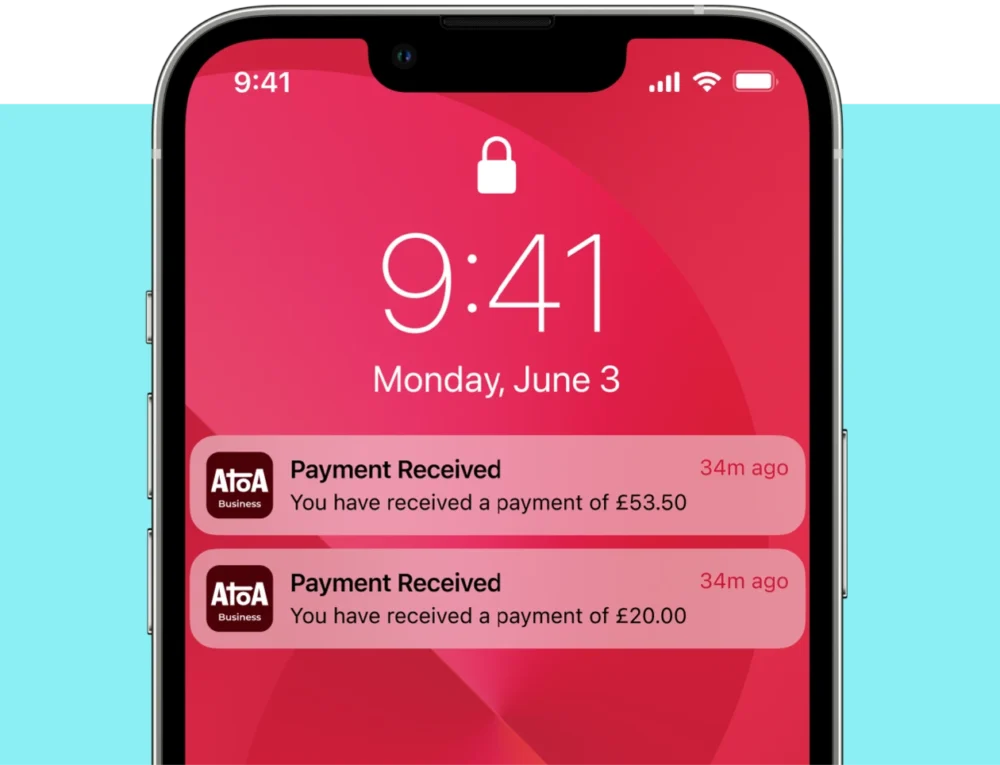

- Real-time confirmation: Businesses are notified instantly when a payment is completed.

Thanks to open banking and consumer demand for easier mobile payments, Pay by Bank is no longer just a niche option, it’s becoming a modern default. This is bank transfer but with the speed and confidence of new tech.

Common questions and misconceptions

“Will my customers know how to use it?”

Yes. Most UK customers already use mobile banking. They simply make the payment from their own bank app.

“Is it secure?”

Absolutely. It uses bank-grade encryption, plus SCA for every transaction.

“What if I already use cards?”

No problem. Businesses can offer Pay by Bank as an additional option, allowing customers to choose their preferred method.

Why now’s the time to switch (or start offering it)

The landscape is shifting. Card processing fees are rising, and consumer preferences are changing, especially among younger, mobile-first shoppers who expect fast, frictionless ways to pay.

Cash usage is also declining. According to recent data, ATM withdrawals in the UK dropped by 31% since 2019. That’s £100 million less being taken out every day compared to before the pandemic, clear evidence that UK consumers are relying less on cash payments.

With the open banking infrastructure now mature and well-supported in 2025, delaying adoption means clinging to higher fees, slower settlements, and outdated payment methods. Businesses that switch to Pay by Bank now position themselves ahead of the curve, offering something faster, more secure, and in tune with what customers already prefer.

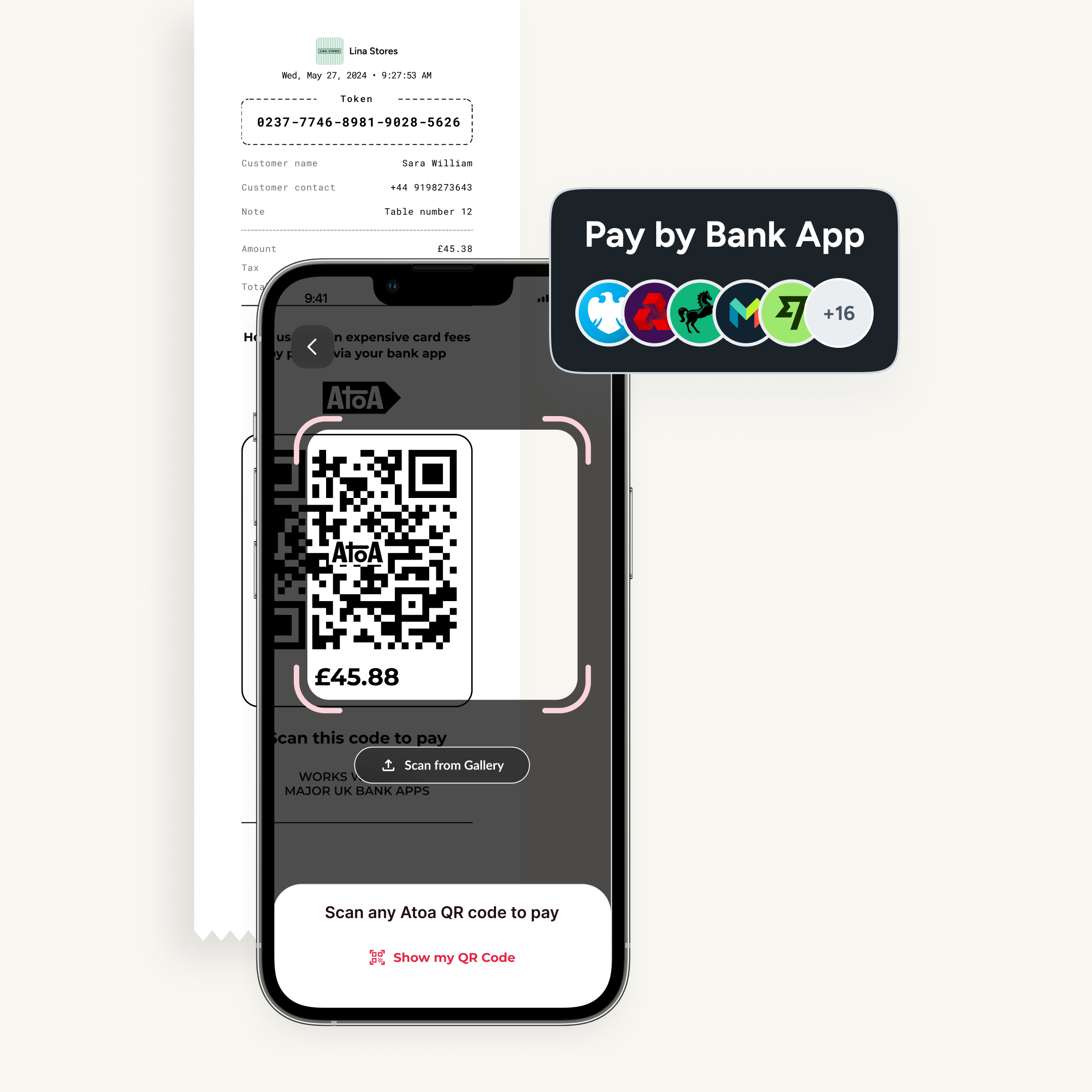

How to start using Pay by Bank

Here’s how you can get started. It’s easier than you think.

- Sign up with a Pay by Bank provider like Atoa.

- Link the business bank account securely.

- Customers can pay with a payment link or scan a QR code at checkout.

- Business is paid instantly, with confirmation in real-time.

Final thoughts

Pay by Bank is more than just a payment method. It’s a shift towards faster, fairer, and more transparent business practices. With instant settlement, lower fees, and bank-grade security, its benefits are real.

Thousands of UK businesses are already using Atoa to power Pay by Bank payments. With minimal operational disruption and easy setup, it’s a practical way to future-proof your payment experience.Looking to explore this further? Book a free demo with the Atoa team and discover how simple it can be to transition to Pay by Bank.