Ready to get started?

Easily integrate next-generation payments and financial data into any app. Build powerful products your customers love.

SHARE ARTICLE

Getting paid shouldn’t be complicated and in 2025, more UK businesses are realising that. Whether you run a car dealership, a salon, or a law firm, payment links are becoming the go-to way to get paid quickly, securely, and without the usual payment drama. Also, it is a simple, convenient way to collect money without needing a website, a card machine, or any awkward payment faff.

So, in this guide, we’ll break down why payment links might just be the smartest way for your business to get paid in 2025.

What are payment links?

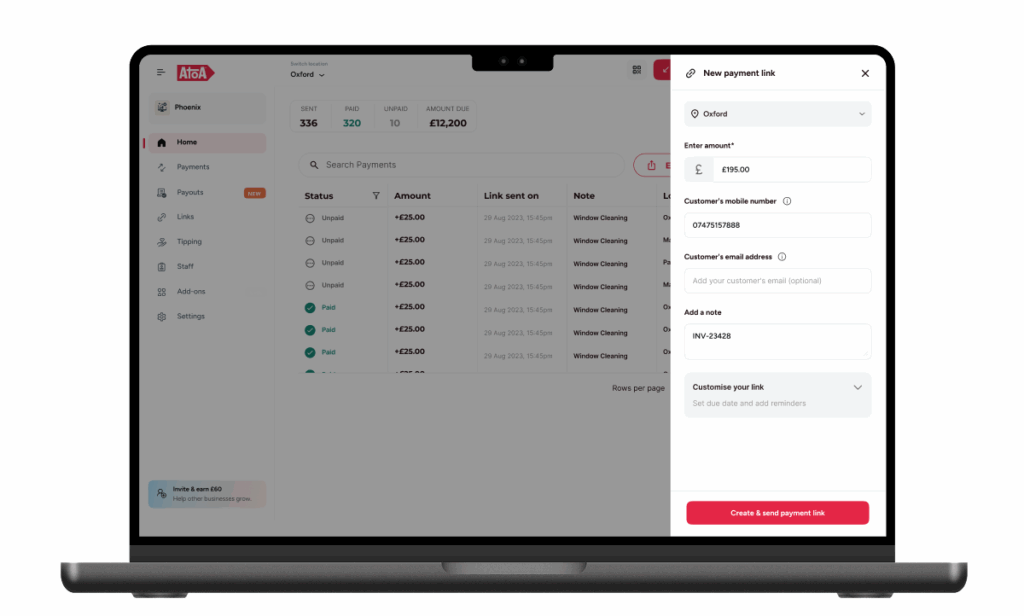

A payment link is a unique URL you can send to a customer so they can pay you online. When the customer clicks the link, they’re taken to a secure checkout page where they can complete the payment using their bank or preferred method.

No apps nor any hardware, and no chasing for bank details. You can send a link by email, text message, WhatsApp, or even Instagram DMs, making it perfect for dynamic businesses.

They’re sometimes also called:

- Link payment

- Payment by link

- Online payment link

- Payment link for businesses

And they all mean the same thing: a simpler way to get paid.

1. Makes getting paid easier… for everyone

One of the biggest benefits of using payment links is how easy they are to use. You don’t need a website, and your customer doesn’t need to download an app or log in to anything.

Just send the link → customer clicks → payment done.

It’s especially useful for:

- Service providers who want to get paid after appointments

- Shops or salons without an e-commerce setup

- Businesses that want to reduce admin

2. Speeds up cash flow

Nobody likes waiting days to get paid. With link payments, customers can pay you as soon as they receive the link and with providers like Atoa, funds can settle instantly in your bank account.

Faster payments = smoother cash flow = fewer sleepless nights worrying about unpaid invoices.

3. Works wherever your customers are

Whether you’re trading online, in-store, or on the move, payment links work across every channel. You can:

- Share them via text, email or social media

- Attach them to invoices

- Display them on QR codes in-store

It’s a flexible option that travels with your business, no matter where or how you work.

4. Cuts down your costs

Card machines come with hidden fees and card payments involve middlemen. Payment links? Not so much. Most Pay by link UK solutions cost less than traditional card processing, with lower transaction fees and no hardware costs. It’s a more transparent way to take payments, especially if overpaying for point-of-sale systems you barely use seems tiring.

5. It’s safe and secure

Reputable payment link providers make sure that every transaction is protected. With open banking-powered providers like Atoa, customers pay through their bank, not by entering card numbers online.

No shared card details = less risk of fraud.

It’s also PSD2 and SCA-compliant (Strong Customer Authentication).

6. Great for growing businesses

If your business is scaling fast or going hybrid (part in-person, part remote), payment links help you keep up. You can send them in seconds, keep track of all payments in one dashboard, and integrate them with your accounting tools.

They’re also handy if you:

- Don’t want the hassle of setting up a full online store

- Need a lightweight way to take digital payments

- Want to test new sales channels (like WhatsApp, Instagram, or email)

7. Future-proofing your payment process

According to UK Finance, 45% of all business payments in the UK in 2023 were made using remote banking, including online transfers and payment links. Experts expect that number to grow significantly over the next decade as more customers switch to mobile and online banking. Adopting payment links now doesn’t just make your business more efficient today, it gets you ready for the future of payments.

Takeaway

Payment links aren’t just a clever workaround, they’re one of the simplest, most effective upgrades you can make to your payment process. They’re fast, secure, and customer-friendly, helping you reduce costs, boost cash flow, and modernise how your business runs.

Thousands of UK businesses are already enjoying the benefits of payment links with Atoa. Also, it’s easy to set up, doesn’t disrupt your existing systems, and starts working for you from day one. If you’re looking for a better way to get paid, book a demo with the Atoa team.

FAQs about payment links

What is a payment link?

A payment link is a URL you send to customers so they can pay you online. Once they click on the link, it then opens a secure checkout page where they can approve the payment.

Can I use payment links without a website?

Absolutely. It’s one of their biggest advantages, so you don’t need an online store to accept payments.

What kind of businesses can use payment links?

Any registered business in the UK can use payment links. If your customer has a phone or email, you can send them a link and collect payments instantly.

How do I start sending payment links?

With brands like Atoa, it only takes a few minutes. So, sign up, generate a link, and start collecting payments straight to your bank account.