Ready to get started?

Easily integrate next-generation payments and financial data into any app. Build powerful products your customers love.

SHARE ARTICLE

Every payment your customer makes costs you something. Not a lot per transaction but multiply it by hundreds of orders a month and it becomes a real number on your P&L. The good news is that the options available to UK online stores have expanded considerably. And the smartest approach in 2025 isn’t about finding one perfect gateway. It’s about offering the right mix.

Here’s how the major providers stack up, and where Pay by Bank fits in.

What payment processing actually costs

UK online card fees typically range from 1.5% to 3.5% per transaction, with the exact figure depending on your provider, plan tier, card type, and whether the customer is paying domestically or from abroad.

A snapshot of current rates for popular providers:

| Provider | UK Card Fee | Best For |

|---|---|---|

| Stripe | 1.5% + £0.20 | Developer-friendly, global reach |

| Shopify Payments (Basic) | 2.0% + £0.25 | Shopify stores wanting native integration |

| Shopify Payments (Advanced) | 1.5% + £0.25 | Higher-volume Shopify stores |

| Wise Business | 1% domestic / 2.9% international | Multi-currency, cross-border sellers |

| Checkout.com | Custom / quote-based | Enterprise and high-volume merchants |

| Atoa (Pay by Bank + Cards) | Competitive card rates + lower Pay by Bank fees | UK businesses wanting both options on one platform |

A few things worth noting on these. Shopify Payments fees reduce as you move up plan tiers, but the monthly subscription cost increases too, so it only makes sense at higher volumes. Checkout.com doesn’t publicly list pricing; it’s custom-quoted based on your business profile and volume, and tends to suit larger merchants. Wise is more of a multi-currency business account than a checkout gateway, excellent for cross-border payments and FX, but not built for a traditional ecommerce checkout page.

Where Pay by Bank changes the calculation

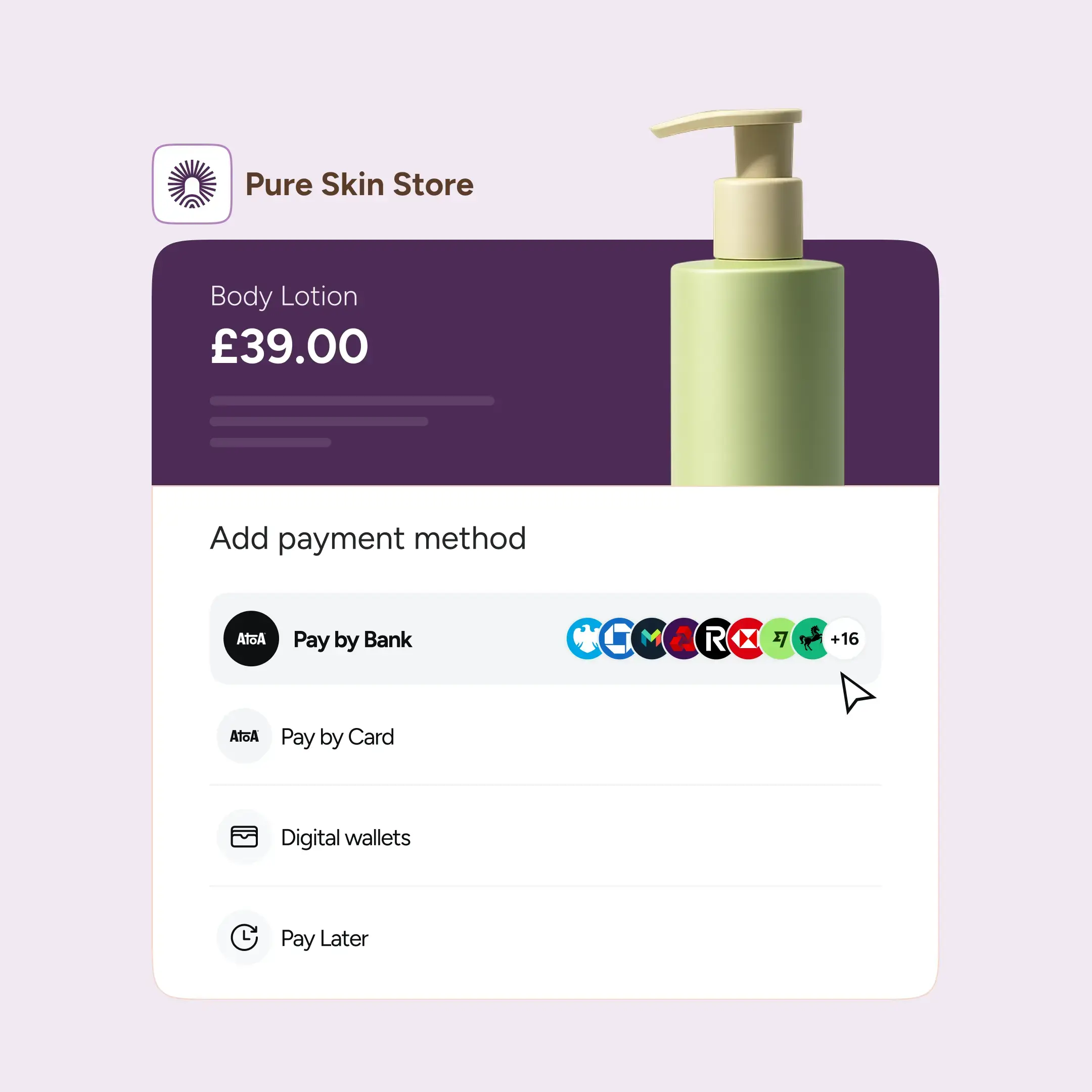

Pay by Bank is a payment method that lets customers pay directly from their UK bank account, bypassing card networks entirely. The customer selects Pay by Bank at checkout, authenticates inside their banking app using Face ID or fingerprint, and the payment lands in the merchant’s account almost instantly via the UK Faster Payments network.

Because no card network is involved, the fee structure is fundamentally different. According to Open Banking Limited’s 2025 Impact Report, there are now 13.3 million active open banking users in the UK, with payments growing 70% year on year, so offering it alongside cards is increasingly a sensible checkout decision, not a niche one.

Pay by Bank also removes chargeback risk entirely. Payments are approved directly by the customer’s bank using Strong Customer Authentication. This means no disputed transactions of the card chargeback type.

Why flexible payments win

The most cost-effective approach for most UK online stores isn’t to replace cards, it’s to add Pay by Bank alongside them. Customers who prefer cards keep that option. Customers who are happy to pay from their bank account use the lower-cost route. Over time, as Pay by Bank adoption continues to grow, that mix shifts in a direction that’s better for your margins.

Atoa offers exactly this: Pay by Bank and card payments on one platform, with a single integration. For UK ecommerce businesses that want to reduce payment processing costs without removing familiar checkout options. It’s a practical starting point.Book a demo with our team to get first-hand experience of this flexible payment platform.