Ready to get started?

Easily integrate next-generation payments and financial data into any app. Build powerful products your customers love.

SHARE ARTICLE

If you run a consultancy, accountancy practice, law firm, or any other professional services business in the UK, you already know the drill: the work gets done, the invoice goes out, and then you wait. According to Funding Circle’s analysis, professional services is the second most affected sector for late-payment-related business closures in the UK, with 1,855 firms estimated to have shut in 2024 because of delayed invoices. Late payments are not a cash flow quirk. For many firms, they are an existential risk.

The right Xero payment integration UK businesses choose can change this dynamic considerably. When clients can pay directly from an invoice with one click, Xero invoice automation handles reconciliation in the background, and your team stops spending hours chasing what they are already owed.

Here is how the main Xero payment gateway options compare.

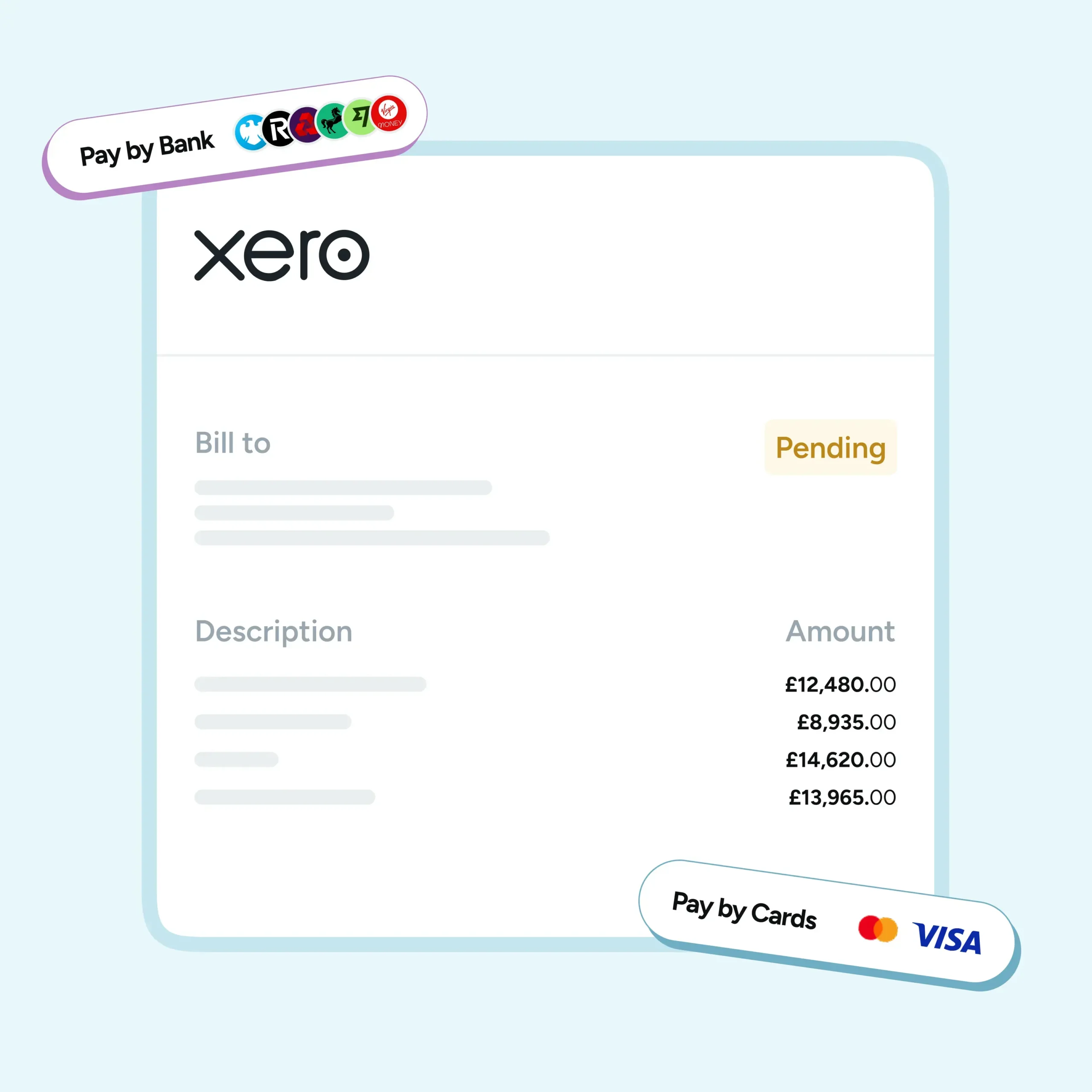

Atoa (Pay by Bank and cards)

Atoa integrates directly with Xero invoices, giving clients two ways to pay from the same payment link: Pay by Bank or card. When a client clicks “Pay now” on their invoice, they can either pay directly from their UK banking app via open banking or choose to pay by card. Funds arrive quickly, the invoice marks as paid in Xero automatically, and reconciliation takes care of itself.

Pay by Bank bypasses card networks entirely, which means lower fees per transaction compared to card-only options. It also removes chargeback risk, which matters when invoice values are significant. Card payments sit alongside it for clients who prefer that route. Atoa is FCA-authorised and built specifically for UK businesses. Note that an additional 10p per transaction applies to Xero invoice payments.

Stripe

Stripe is Xero’s default card integration and the most established option for card-only payments. A “Pay now” button appears on every invoice, supporting credit cards, debit cards, Apple Pay, and Google Pay, with automatic reconciliation in Xero.

UK domestic card fees run from 1.5% + £0.20 for standard consumer cards, rising to 2.5% + £0.20 for EU cards. Stripe is reliable and widely trusted, but the fees are worth keeping an eye on as invoice values grow.

GoCardless

GoCardless is the go-to for firms with recurring retainer clients. It handles Direct Debit rather than card payments, with fees starting from 1% + £0.20 per domestic transaction, capped at £4. The limitation is that clients need to set up a mandate first, and payments take a few days to clear, making it less suited to one-off project invoices.

PayPal

PayPal is an option, but at 2.9% + £0.30 per transaction it is the most expensive on this list. It is familiar to most clients, but harder to justify for B2B invoice payments where the sums involved make the fee difference more noticeable.

Choosing the right setup

Running Atoa alongside GoCardless covers most professional services firms well. Atoa handles one-off invoices with flexible payment options at lower cost. GoCardless manages recurring clients on Direct Debit. Together, they reduce both transaction fees and the time your team spends chasing payments. For firms looking to modernise their accounting software payments setup without rebuilding their processes, it is one of the more practical combinations available. If you want to see how Atoa works with Xero for your business, book a demo with the Atoa team.