Ready to get started?

Easily integrate next-generation payments and financial data into any app. Build powerful products your customers love.

SHARE ARTICLE

When a customer is about to transfer £18,000 for a vehicle, the payment process stops being a back-office task. It becomes central to the deal.

Payments for automotive dealerships are different from most retail environments. Transaction values are high, fraud exposure is greater, and payment fees scale quickly. A single failed or disputed payment can erase margin on a vehicle sale.

In 2025, the UK new car market rose 3.5 percent to just over 2.02 million registrations, the first time it has crossed two million since 2019. At this scale, even small inefficiencies in dealership payment handling can carry meaningful financial impact.

Why high-value payments in automotive carry more risk

High value payments automotive businesses process every day include:

- Vehicle deposits

- Full balance payments before handover

- Finance settlements

- High-ticket servicing and repairs

In the UK, many dealerships still rely heavily on cards. But card payments on large transactions create predictable problems. Percentage-based fees grow with the vehicle price. Commercial and premium cards cost more. Card limits block larger purchases. And chargebacks on high-value goods are expensive to defend.

This is why reviewing car dealership payment methods UK operators rely on is no longer optional. It is a marginal decision.

The real cost of traditional payment methods

Most dealerships use a mix of:

- Card payments: Convenient, but expensive at scale and exposed to disputes.

- Manual bank transfers: Often require waiting for cleared funds before releasing a vehicle.

- Phone payments: Higher compliance risk and weaker authentication.

Individually, these methods work. But when handling high value payments automotive businesses depend on, they introduce friction and cost that compound over time.

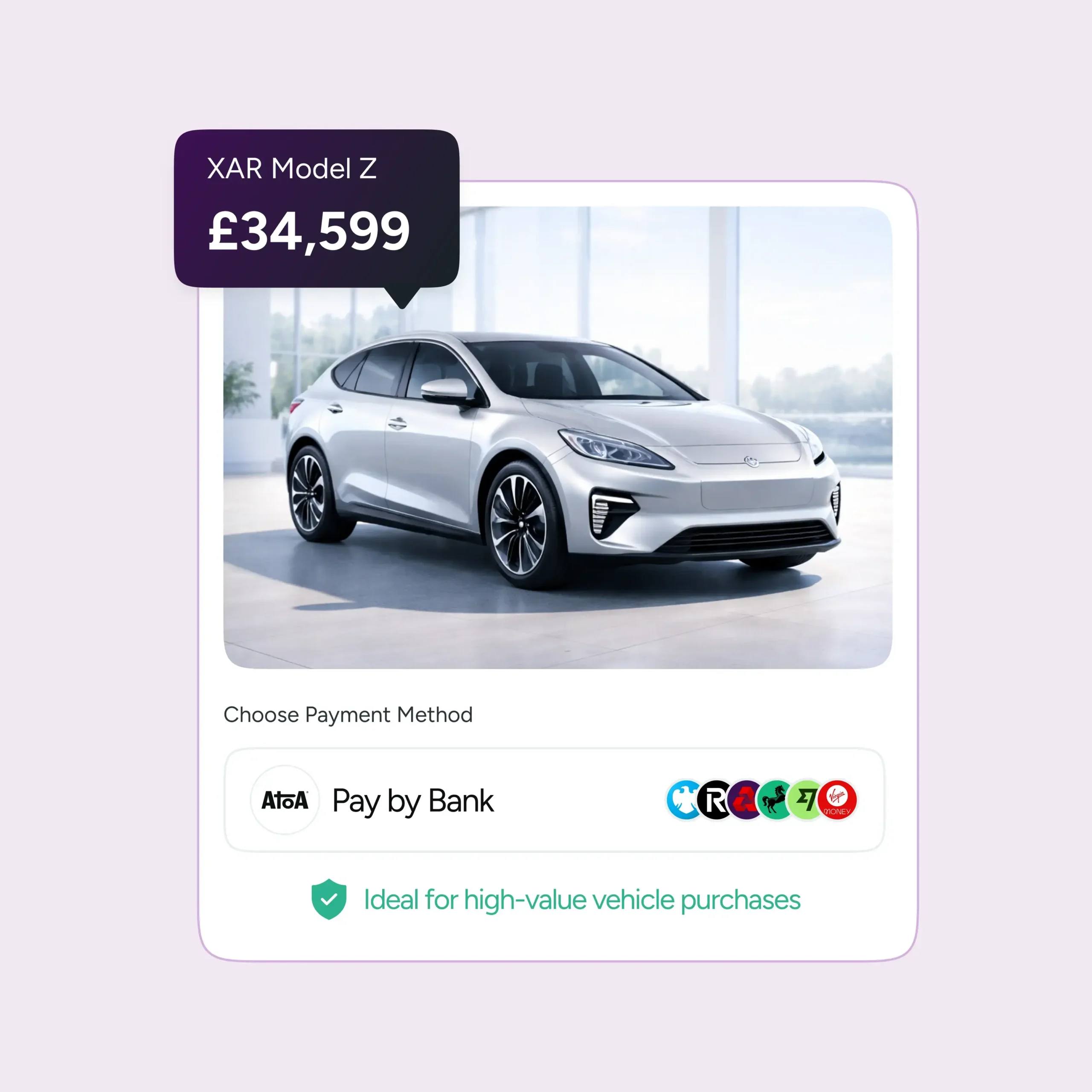

A more secure alternative: Pay by Bank for car dealerships

Pay by Bank car dealerships are increasingly adopting a more secure route for large transactions.

Instead of processing a card, the dealership sends a secure link or presents a QR code. The customer selects their bank and approves the payment inside their own banking app. Funds move directly from bank to bank with real-time confirmation.

This changes several things at once:

- No card limits blocking large purchases

- Lower processing costs compared to percentage-based card fees

- Strong in-app authentication reduces dispute exposure

- Immediate confirmation before vehicle release

For high value payments automotive businesses process daily, this significantly lowers risk.

Security and flexibility together

This is not about removing cards entirely. Dealerships still benefit from offering multiple payment options. Cards remain useful for smaller deposits or customer preference.

But when reviewing payments for automotive dealerships, the question is not convenience alone. It is cost, authentication strength, and operational efficiency.

A balanced approach allows dealerships to:

- Take deposits remotely

- Accept large balance payments securely

- Reduce reconciliation delays

- Protect margin on high-ticket sales

Final thoughts

As vehicle prices rise, payment risk rises with them. The way dealerships handle high value payments automotive transactions involve should reflect that reality.

Relying solely on traditional card flows exposes dealerships to unnecessary fees and dispute risk. Expanding car dealership payment methods UK operators use to include secure bank-based payments offers stronger authentication, lower cost per transaction, and greater operational confidence.If you want to explore how secure bank payments can support payments for automotive dealerships, book a demo with the Atoa team and see how Pay by Bank fits into high-value vehicle sales.