Recurring payments,

without the rigidity

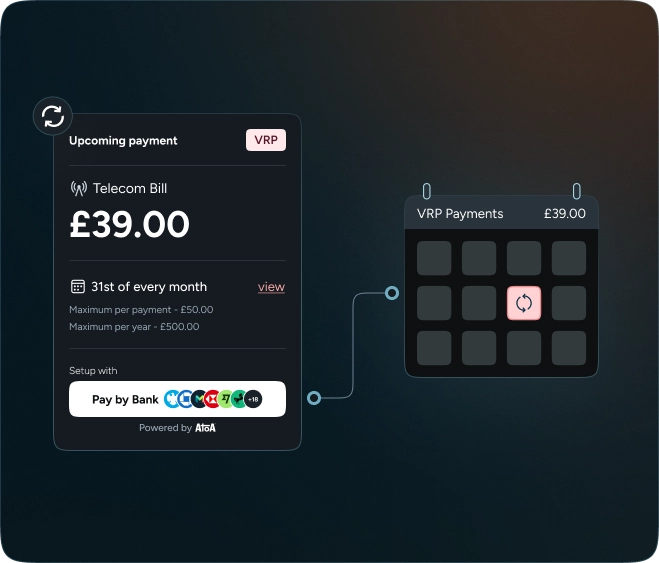

How VRP Works

Commercial Variable Recurring Payments (VRPs) let businesses

securely take repeat payments directly from a customer’s bank account.

Customer authorises in Bank app

Customer approves a payment agreement with set limits

Business triggers payment

You initiate payments within those agreed limits.

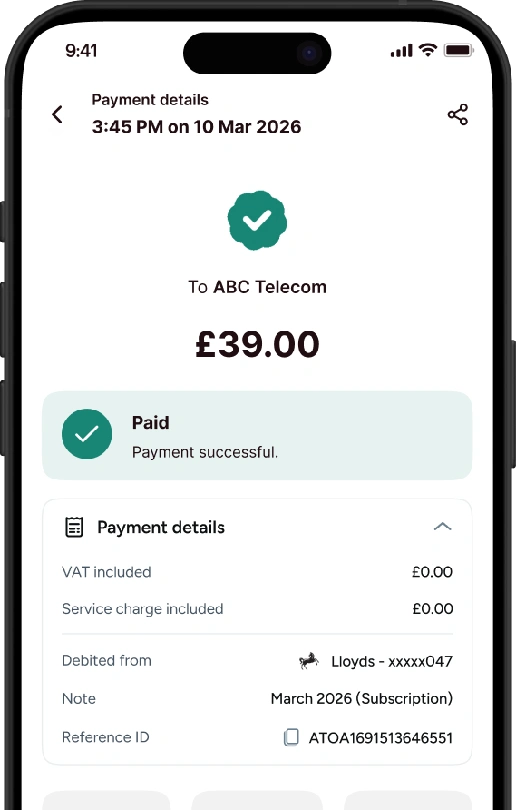

Payment is confirmed

Funds are transferred instantly from their bank to yours.

FCA regulated • ISO & SOC Certified • Security backed by UK banks

Customer authorises in Bank app

Customer approves a payment agreement with set limits

Business triggers payment

You initiate payments within those agreed limits.

Payment is confirmed

Funds are transferred instantly from their bank to yours.

Direct Debits vs VRP

VRP will replace outdated Direct Debit mandates by enabling real-time, flexible, bank-to-bank recurring payments with lower fees and faster settlement.

| Feature | Direct Debit | VRP | Benefit to business |

|---|---|---|---|

| Underlying Rails | Bacs – Batch Clearing | Faster Payents (Real-Time, Account-to-Account) |

Funds hit your account same day (no more 3 day gap) |

| Setup Time | 5-10 working days | Real-Time | Instant setup eliminates drop-off during onboarding, customers from day one |

| Settlement Speed | 3 working days | Real-Time | Immediate settlement boosts business cash flow and reduces non-payment risk |

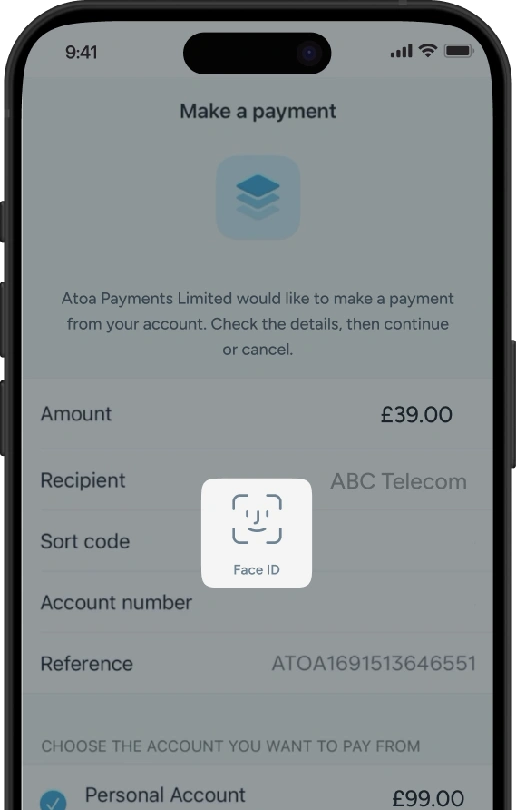

| Authorisation Method | Paper signature or digital form | Strong customer authentication (Face ID, Fingerprint Scan) |

SCA reduces fraud and chargeback risk; bank grade auth shifts liability away from merchant |

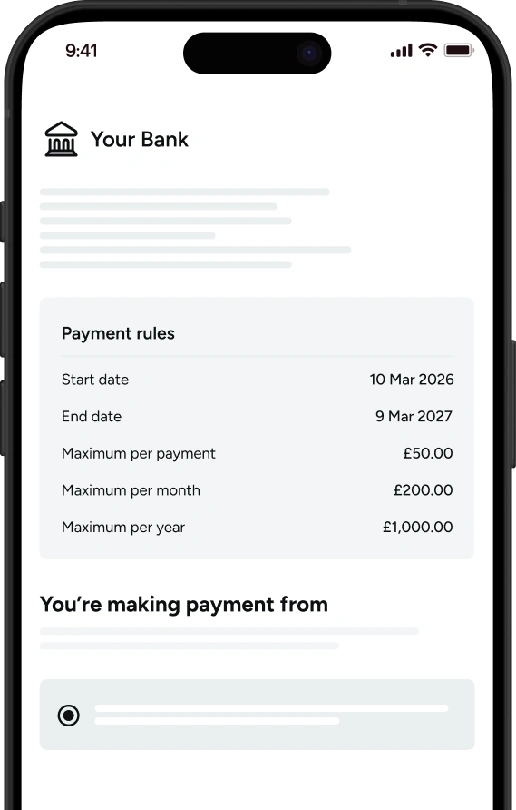

| Advance Notice | Minimum 10 working days before a change in amount/date/ frequency can occur |

Not required if the change is within the original consent parameters |

Collect usage-based charges instantly |

| Dispute Window | No statutory time limit (can go on for months) |

Faster than DD timelines | Faster dispute resolution reduces cash tied up in contested payments |

| Data Shared with Merchant | Full name, account number, sort code | Minimal – amount + merchant name | Less PII to store means lower GDPR compliance burden and reduced data breach risk |

| Cancellation Speed | 2-3 working days | Instant via Bank App | Customer-friendly cancellation builds trust; reduces complaints and support tickets |

| Failed Payment Handling | Notification after 3-day cycle | Instant failure notification | Instant failure alerts cut recovery costs and let you retry or escalate the same day. |

(Real-Time, Account-to-Account)

(no more 3 day gap)

(Face ID, Fingerprint Scan)

frequency can occur

the original consent parameters

(can go on for months)

Where VRPs work best

Utilities

Collect variable bills for electricity, gas, water, and telecom services each cycle, within approved limits.

Government services

Collect council tax, licensing fees, or charges within defined limits, directly from bank accounts.

Charities

Allow donors to give recurring donations where the amount may vary each month.

Financial services

Regulated firms can collect recurring payment for use cases such as insurance premiums, and loan repayments.

Other Business Types (Later)

Businesses will be able to collect monthly recurring subscriptions such as gym membership or monthly service plans.

Online Retail (Later)

Businesses will be able to collect variable recurring payments where the total changes each month based on usage.

A trusted partner

for businesses in the UK

See how much you can save with Pay by Bank

- Up to 50% lower payment fees

- Faster access to funds

- One platform for modern payments

ISO-27001 and SOC2 Secure

Security backed by UK banks

Authorised by the FCA

Schedule a quick chat with our team!

Select your preferred time, and our team will give you a short demonstration of how Atoa can work for your business. Book a call

Book a callVRPs are a new way to collect recurring payments using open banking.

Your customer approves a payment agreement once in their banking app, with clear limits (like how much you can take and how often). After that, you can collect payments within those limits without asking them to approve every time.

Payments are sent instantly from their bank to yours, with no cards involved.

You set up a VRP agreement in your Atoa dashboard by choosing things like the amount, frequency, and limits.

Your customer then:

- Receives a secure link

- Approves the agreement in their banking app

Once that’s done, you can collect payments automatically within the agreed limits.

No chasing. No re-authentication. Funds arrive instantly.

VRPs are faster, more flexible, and more transparent.

- No waiting days for setup or settlement

- Instant confirmation if a payment succeeds or fails

- No need to send advance notice for amount changes

- No handling of sensitive information like account numbers or sort codes

In short, you get paid quicker and spend less time managing failed payments.

Yes, security is built in from the start.

Customers approve the agreement directly through their bank using Strong Customer Authentication (e.g. Face ID or fingerprint), which is significantly more secure than traditional Direct Debit mandates that can be set up using just bank details.

You never see or store sensitive bank information, reducing your compliance burden as well.

Customers with supported UK banks can pay via VRP. This includes major banks like HSBC, Barclays, Lloyds, NatWest, Monzo, Revolut, and Starling.

More banks are being added as VRPs roll out.

If a customer’s bank isn’t supported, Atoa will offer other payment options like Pay by Bank or card.

Customers can cancel their agreement anytime from their banking app.

You’ll be notified straight away in your Atoa dashboard, so you can follow up or switch them to another payment method.

Because customers stay in control, you’ll spend less time handling payment disputes.

VRPs are expected to launch in the second half of 2026.

We’re currently testing to make sure everything works smoothly from day one. If you’d like early access, you can register your interest with our team.

Pricing will be shared closer to launch.

That said, VRPs are designed to be a cost-effective alternative to Direct Debit. You benefit from:

- Faster access to funds

- Immediate visibility on failed payments

- Less admin chasing payments

For many businesses, that means lower overall costs, not just lower fees.

VRP is launching in waves. The first wave covers four regulated sectors: utilities (electricity, gas, water, and telecom), government services (council tax and licensing fees), financial services (insurance premiums and loan repayments), and charities (recurring donations). If your business falls into one of these categories, you can start collecting variable recurring payments as soon as we go live by early Summer 2026.

Subscriptions (such as gym memberships and monthly service plans) and online retail (where the payment amount changes based on usage) will launch later this year. We’ll update this page as new categories go live.